CRED: A Business Model that can't fail

Ever since it was launched in November 2018, the credit card payment app Cred has been building buzz. This may be in Kunal Shah's ads as founder or funding, but more importantly about the CRED business model (the hot topic).

Ever since it was launched in November 2018, the credit card payment app Cred has been building buzz. This may be in Kunal Shah's ads as founder or funding, but more importantly about the CRED business model (the hot topic).

First, let's look at the Funding & Financials before moving to the hot topic:

- In June 2018, CRED raised a $30M seed round from Sequoia India, Ru-Net & Ribbit Capital.

- In April 2019, it followed by a $25M Series A led by angels Sriram Krishnan, Amrish Rau, Akshay Kothari, Sriharsha Majety, Jitendra Gupta + more as well as a couple of early venture funds including Rainmatter (Zerodha's Fintech fund), Ganesh Ventures, Whiteboard Capital among others.

- In Aug 2019, it raised a $120M Series B funding led by Sequoia India, Ribbit Capital & Gemini Investments with further participation from Tiger Global, Hillhouse Capital, General Catalyst, Greenoaks Capital, and Dragoneer.

- In Jan 2021, Cred has raised a fresh $81 million as part of its Series C funding round led by existing investor DST Global also saw participation from Sequoia Capital, Ribbit Capital, Tiger Global, and General Catalyst.

It brings the total funds raised to $228m across four rounds, including $1m in seeding from founder Kunal Shah, and inches the burgeoning startup towards unicorn status with a post-money valuation above $800m in Jan 2021.

CRED's operations data

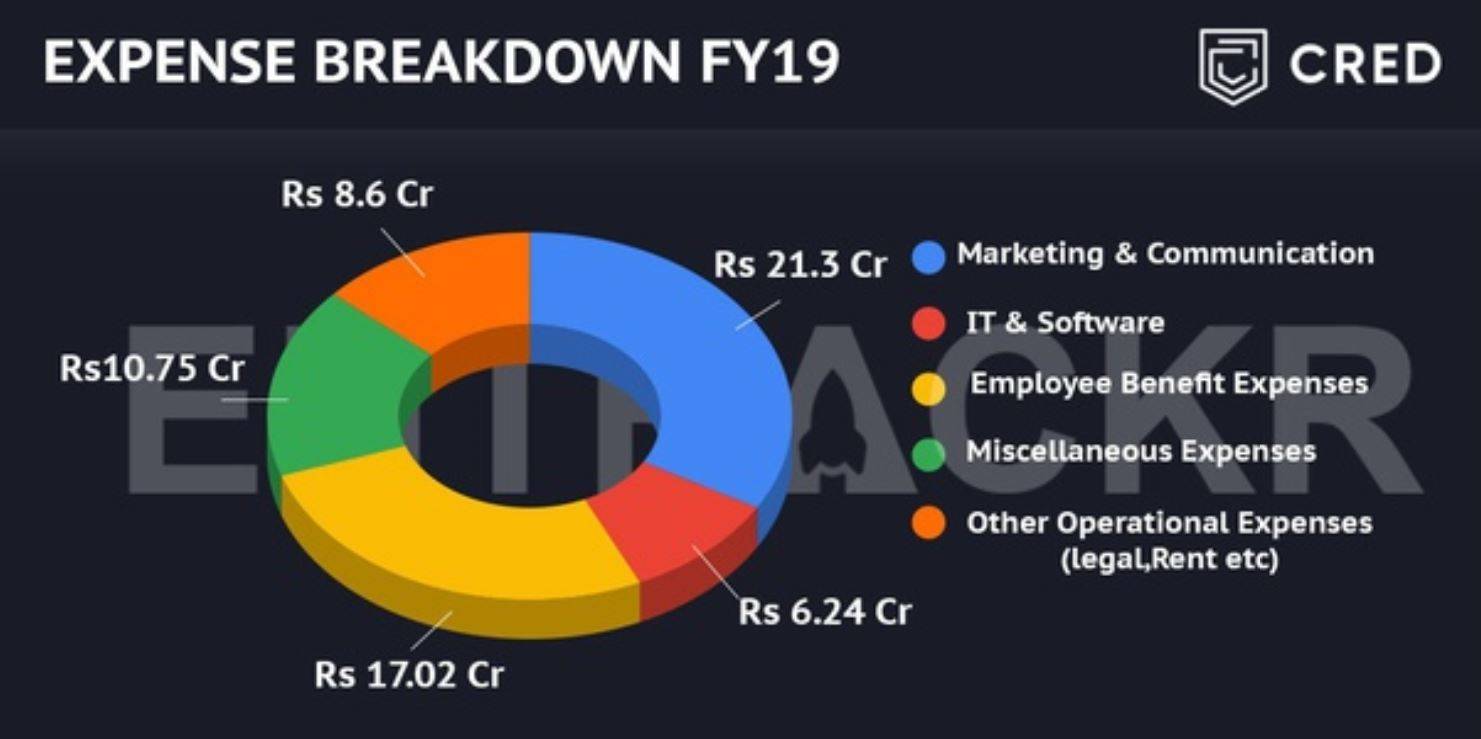

In FY19 (April 2018 - March 2019) operated for just 5 months,

Total expenses = Rs.64 Cr

Revenue = Rs.3 Cr (from interest on deposits - one way of revenue generation)

Total Loss = Rs.61 Cr (Marketing & Communications & Employee Benefits were the company's core expenses amounting to ₹38 Cr)

![]()

So does CRED has an existential crisis? If no then what is the business model in Kunal Shah’s mind?

Let’s try to find out the business model of CRED. The fact is CRED has access to an enormous amount of capital due to a lot of transactions that take place and is building financial products for the 1% of India with a large premium engaged member base.

Size of the market and the kind of consumer CRED largely targets

Mr Sajith Pai (Director, Blume Ventures) has a great piece on compartmentalizing the Indian market chiefly into 3 markets:

- India1

- India2

- India3

- India1 corresponds to the richest 110M Indians who make up $1T of India's GDP. India1 also has a smaller subset of the richest 10M which is its own market and can be called India 1α.

- CRED largely targets this consumer base. These are the folks who own iPhones, holiday in the US or Europe, send their children to study in elite private schools, frequently use DTC products, and most importantly (for CRED) own and use their credit cards.

India has about 50M credit cards that have been issued, used by about 25M people with an average monthly credit card spend of Rs.12,000/-. CRED also, through their branding, seems like a millennial-first company targeting the young adult population who are earning comfortably (20M Indians made more than 5L in 2018-2019).

CRED's product journey can be split up into three stages:

- Rewarding Consumers

- Building Trust With Consumers

- Delighting Consumers & Monetization

Rewarding Consumers

The game-changer business model that CRED took early on was to reward its users for paying bills on time. This message helped to acquire a lot of users.

Interesting right!!! You get rewarded for being good.

When you pay your credit card bill(s) on CRED you get 1 CRED coin for every rupee you spent.

Earn money for spending money!

Building Trust With Consumers

CRED, a high-trust community of creditworthy individuals, merchants, and institutions, has reimagined the CRED experience with its 4 products aimed at increasing financial confidence for creditworthy individuals.

- CRED Stash

An instant credit line up to ₹5L, Stash is the easiest way to get credit in India in a completely digital manner. CRED rolled this out in a partnership with IDFC Bank, users can access any amount within their available limit, select their payback term and receive the amount in their bank. Users are charged interest on the amount withdrawn & are only charged a third of the interest rates on credit cards. - RentPay

A way for members to pay their monthly rent to landlords with their credit cards. All you need to do is add the amount, your landlord's Bank Account/UPI details, and choose a card to play with. CRED does charge a nominal service fee (up to 1.7%) for the service. The company hopes to earn revenue by charging a fee for using Rentpay - Discover

Selling products and experiences & services in the discover section. It will charge a fee from brands to list their products on the 'Discover' platform where the users can spend CRED coins to avail discounts. Owning the E2E flow of purchasing a product (and using CRED coins for a % of the amount) within CRED would result in much better outcomes for both the merchant & the members. - CRED Pay

It enables brands to create a direct-to-consumer channel by offering them an instant payment experience on their platforms, reducing their dependence on other avenues to sell products and services. Using CRED coins as an incentive for CRED members also helps brands save up on additional advertising costs that they would otherwise bear on traditional pay per click models. It also helps emerging brands access and engage high-spending CRED members who have a high lifetime value and drive the majority of consumption on most platforms.

I can imagine CRED might roll out other credit & financial products in the future (insurance, wealth management in premium offerings).

Now CRED has a community of the richest and most creditworthy individuals, a thriving marketplace with premium products and services, and their own credit card product & membership with better digital & physical rewards.

What we can expect in the future from CRED?

- CRED could build a product that makes the credit card checkout process as seamless & intuitive as using Google Pay or PhonePe since they already have it within the app to pay for products & services.

- They can take their internal payment service (pay with card + CRED coins) and offers it to online businesses and marketplaces (this is what American Express has with Express Checkout). It gives consumers an easy way to use the credit card and utilize their CRED coins, while it ensures a lower fraud rate for the merchant (CRED is accountable for having trustworthy members on their platform).

If you were shopping on Flipkart and were able to pay seamlessly with your credit card through CRED and also use some of your coins to reduce the price, why wouldn’t you use it?

Slowly CRED will become so deeply integrated into your life while making purchases and CRED can extract a lot more value from their members while simplifying their lives and making it easier to do & manage all their spending.

In only 24 months of operations, CRED already processes about $1B in monthly credit card payments in India (12.5% of the total credit card payments), and over time they will continue to conquer the market.

If CRED can't build a profitable financial behemoth in India despite having people who spend the most amount of money in the country, no one can.